Skip to content

Home

Insurance

Expand

Life Insurance

Hairstyles

Search

Toggle Menu

Search

Life Insurance Awareness Month October

101 Insurance Marketing Ideas, Tips, Secrets and Strategies

Senior Life Insurance: How to Navigate the Options If You’re Over 50

The Importance of Life Insurance as a Millennial: A Comprehensive Guide

A Comprehensive Guide to Life Insurance: Benefits, Types, and How It Works

Top 10 Life Insurance Myths

Best Whole Life Insurance Companies in USA

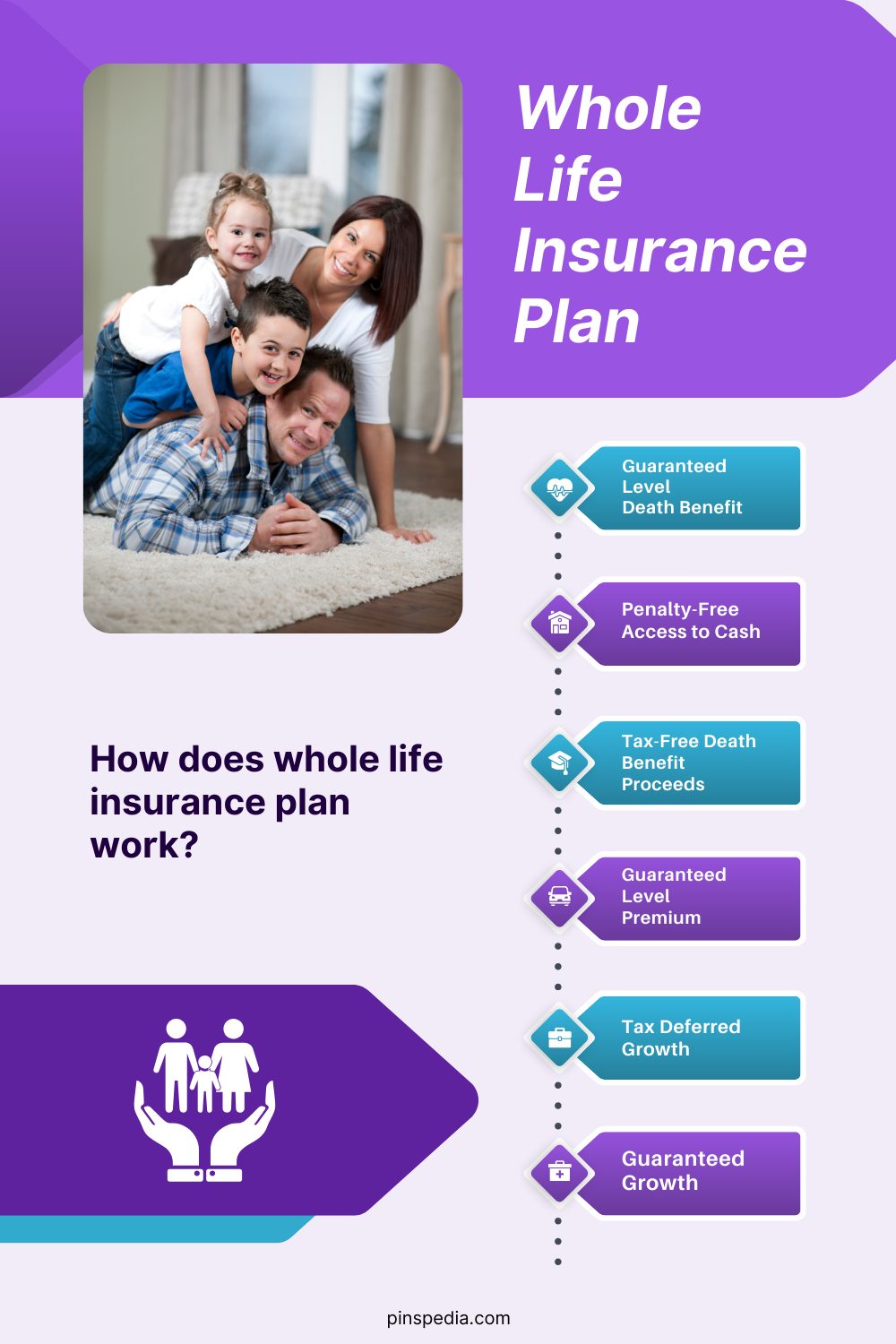

How to Use Whole Life Insurance?

Whole Life Insurance Plan

21 Whole Life Insurance Quotes

Whole Life Insurance for Kids: A Comprehensive Guide

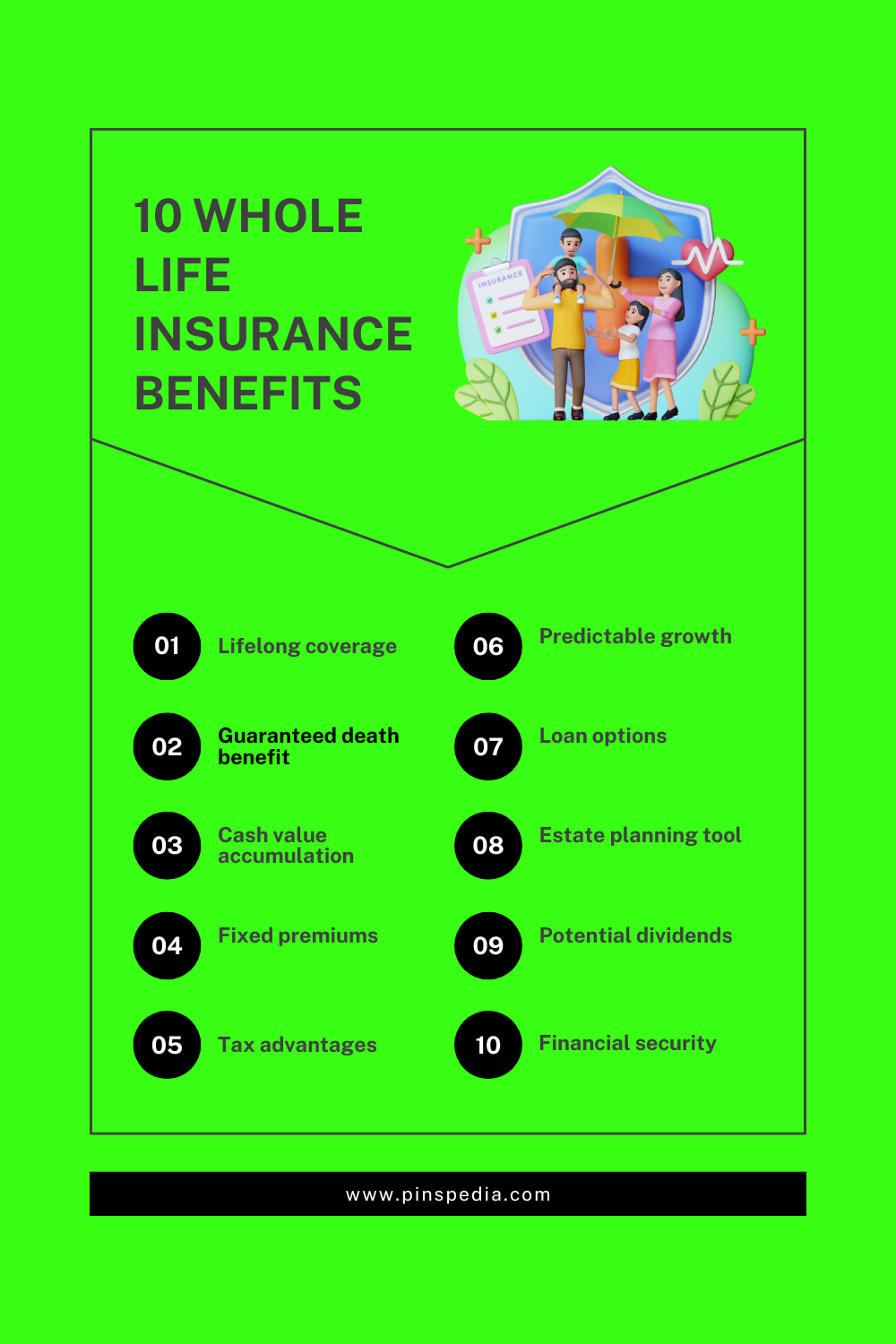

Whole Life Insurance Benefits

Page navigation

Previous Page

Previous

1

2

3

4

5

Next Page

Next

Scroll to top

Scroll to top

Home

Insurance

Toggle child menu

Expand

Life Insurance

Hairstyles

Toggle Menu Close

Search for:

Search