Top Life Insurance Statistics

The state of the life insurance industry is continuously evolving, and understanding trends and changes can help you choose the right policy. Life insurance offers financial support for your dependents after you pass away, helping them cover your final expenses and outstanding debts, such as mortgages or student loans.

In this article, we presented an overview of the most compelling life insurance statistics going into the new year, using data from sources like the American Council of Life Insurers (ACLI), Life Insurance Marketing and Research Association (LIMRA) and the Insurance Information Institute (Triple-I).

If you are interested in purchasing a life insurance policy, consider your financial condition and future goals to find the best life insurance for your needs.

Key Life Insurance Statistics

- A study by the LIMRA and Life Happens shows that in 2023, the percentage of people who reported having life insurance increased to 52%, up from 50% in the previous year.

- Over the past 12 years, there has been a decrease in overall life insurance ownership, dropping from 63% in 2011.

- About 100 million Americans are either without life insurance or inadequately insured, acknowledging their need for additional coverage, according to data from LIMRA.

- A record high of 30% of consumers have indicated their intention to buy life insurance in the upcoming year, also according to LIMRA data.

- Another LIMRA study found that the primary reason for owning life insurance is to fund funeral or burial and other end-of-life expenses.

- Data from Aflac shows that, on average, life insurance policies pay out $168,000, but this amount can vary significantly based on the policy.

- According to the Triple-I, in 2022, the total amount of life insurance benefits and claims amounted to $797.7 billion.

- Based on data from the ACLI and our research, Delaware has the highest average life insurance payout per enforced policy, with an average amount of $4,149.

How Much Does Life Insurance Cost?

The cost of a life insurance policy depends on several factors, including age, gender, medical history, lifestyle and your chosen coverage amount. This means your premium will differ from average policy costs. The following figures and statistics can help you make informed decisions regarding the best life insurance option for your situation.

- The above-cited LIMRA study shows that 42% of consumers do not purchase life insurance because of its high cost.

- Additionally, over half of Americans overestimate the cost of life insurance, believing it to be three times more expensive than it is. This is why it’s important to understand how insurers calculate the cost of life insurance.

- Based on our research, the average monthly premium for a 35-year-old man with a $500,000 policy is $26.

- According to LIMRA, 38% of Americans reported that their household would face financial difficulties within six months if a breadwinner were to pass away, with 30% facing such challenges within a month.

What Are the Different Types of Life Insurance?

You can choose from many types of life insurance, each with its unique features and benefits. Knowing about different options can help you decide which suits you best based on your needs. Here are the main types of life insurance available in the market:

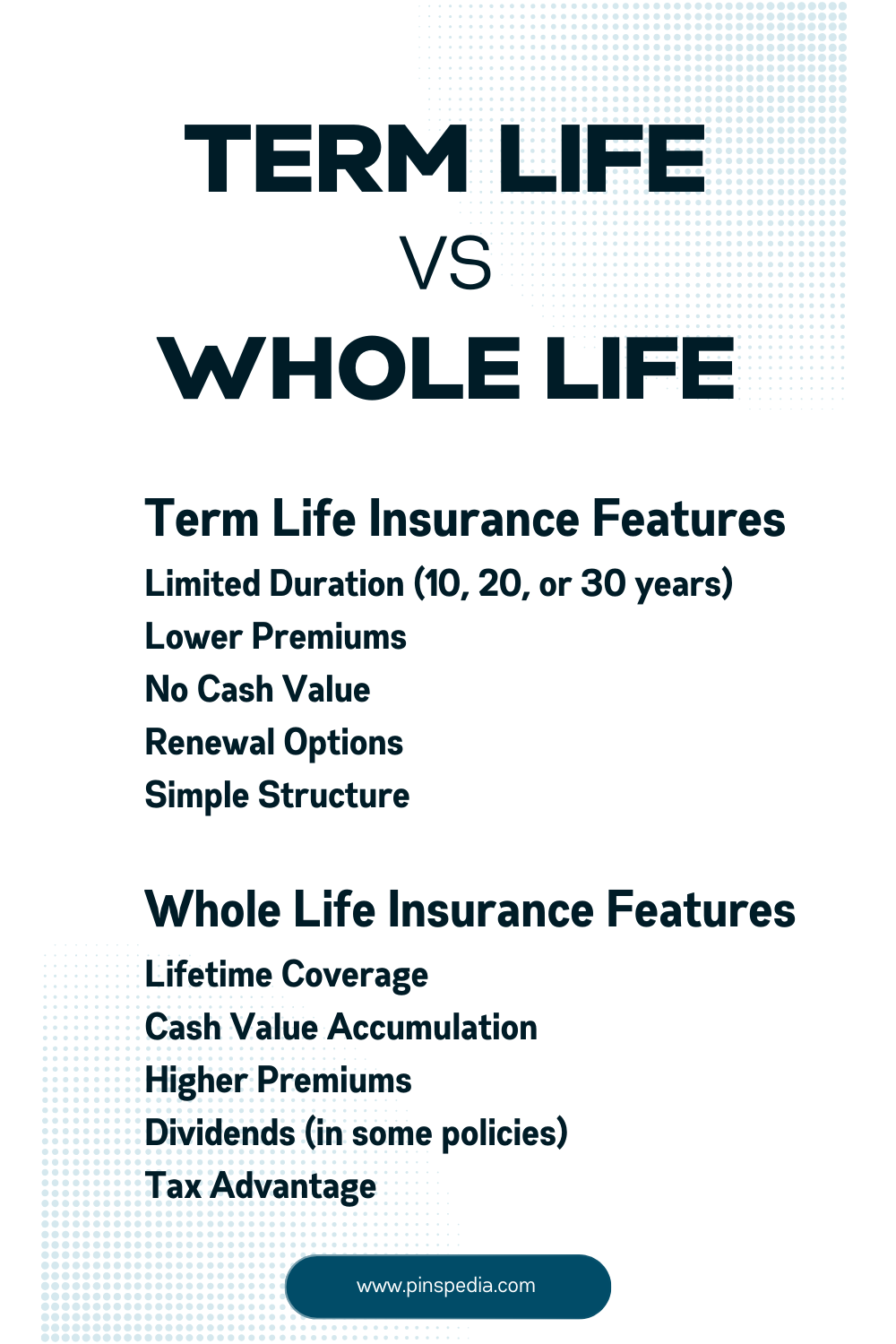

- Term life insurance: This type of policy will cover you for a specific period, such as 10, 20 or 30 years. It has low premiums and is ideal for those seeking coverage for a limited time or to meet a specific financial goal.

- Whole life insurance: A whole life policy includes lifelong coverage, a death benefit and a cash value component. It costs more but will suit those who want permanent coverage and to accumulate cash value.

- Universal life insurance: Similar to a whole life policy, universal life insurance provides lifelong coverage but has flexible premiums and death benefits. Its cash value grows according to a specified interest rate and is best for those who want to be able to modify their policy.

- Variable life insurance: This policy type is riskier than other forms of permanent coverage as its cash value is invested in various accounts and can fluctuate based on performance. However, it offers a higher growth potential than other options.

- Group life insurance: A group life plan has lower premiums and coverage is generally easier to qualify for, often without a health exam. You can get it through your employer as part of your benefits package.

Life Insurance Demographic Trends

Coverage preferences for life insurance can vary based on age groups, genders, socioeconomic backgrounds and other factors. The following trends, which we obtained from the above-mentioned LIMRA study, can give you key insights into the relationship between demographic factors and insurance choices.

- The LIMRA study found that Hispanic Americans have a lower rate of life insurance ownership, with 45% reporting they have coverage, which is below the rates for other racial and ethnic groups.

- While 41% of single mothers own life insurance, a higher percentage (59%) recognize the need for buying life insurance or enhancing existing coverage.

- Life insurance ownership among women is lower compared to men, with 49% of women owning a policy as opposed to 55% of men. This trend marks the fifth consecutive year of declining life insurance ownership among women.

- The percentage of parents who own life insurance has increased to 59%, rising from 54% in the previous year.

- In 2023, for the first time, consumers expressed a preference for buying life insurance online rather than through in-person meetings. Facebook (62%) and YouTube (58%) emerged as the most popular platforms to find insurance information.

- The 2023 Insurance Barometer Study shows that in the next year, a greater percentage of younger demographics, with 44% of Gen Z and 50% of millennials, intend to buy life insurance, surpassing the national average.

Life Insurance Policy Statistics

Knowing which types of policies are popular among consumers can help you understand the current state of the insurance market. Here are some policy statistics related to life insurance:

- Data from the ACLI shows that in 2022, term life insurance accounted for 39.3% of all life insurance purchases.

- Term life insurance represented a substantial 70.5% of the total face amount issued for individual life policies, totaling $1.3 trillion.

- In 2022, permanent life insurance policies made up 60.7% of all life insurance purchases.

Life Insurance Industry Statistics

We gathered the following trends to give you an idea of market changes within the life insurance industry.

- Quarterly data from LIMRA shows that year-over-year from 2022, the sale of life insurance policies has increased by 4%.

- Year-over-year, the total new annualized premium for individual life insurance rose by 5%, reaching $3.7 billion.

- Based on data from Triple-I, independent agents hold a 52% share of the individual life insurance market, while affiliated agents control 38% of the market.

- In 2020, the combined total of life insurance, annuity cash and invested assets amounted to $4.7 trillion, according to the Triple-I.

- Life insurance companies allocated 70% of assets to bonds and 3% to corporate stocks.

State-by-State Breakdown of Life Insurance Ownership

The map and chart below showcase average life insurance payouts across different states. This detailed view can help you understand how your location may impact the benefits your dependents receive with your life insurance policy.

| State | Life Insurance Payout Per Policy In Force |

|---|---|

| Alabama | $750 |

| Alaska | $2,006 |

| Arizona | $2,556 |

| Arkansas | $1,333 |

| California | $2,243 |

| Colorado | $2,053 |

| Connecticut | $3,615 |

| Delaware | $4,149 |

| District of Columbia | $2,442 |

| Florida | $2,213 |

The Bottom Line

A new LIMRA study shows that 39% of consumers plan to purchase life insurance within the following year. If you’re one of them, understanding the trends within the life insurance industry can help you make decisions when choosing a policy. Different types of policies are available and it is best to evaluate your needs to select the right one.

Although you can estimate pricing based on the average cost of life insurance, your actual cost will depend on your situation. Your location significantly affects your premiums and the death benefit your family receives. If you need help selecting a life insurance policy, we recommend speaking with a financial advisor or registered life insurance agent.